The Quick Read

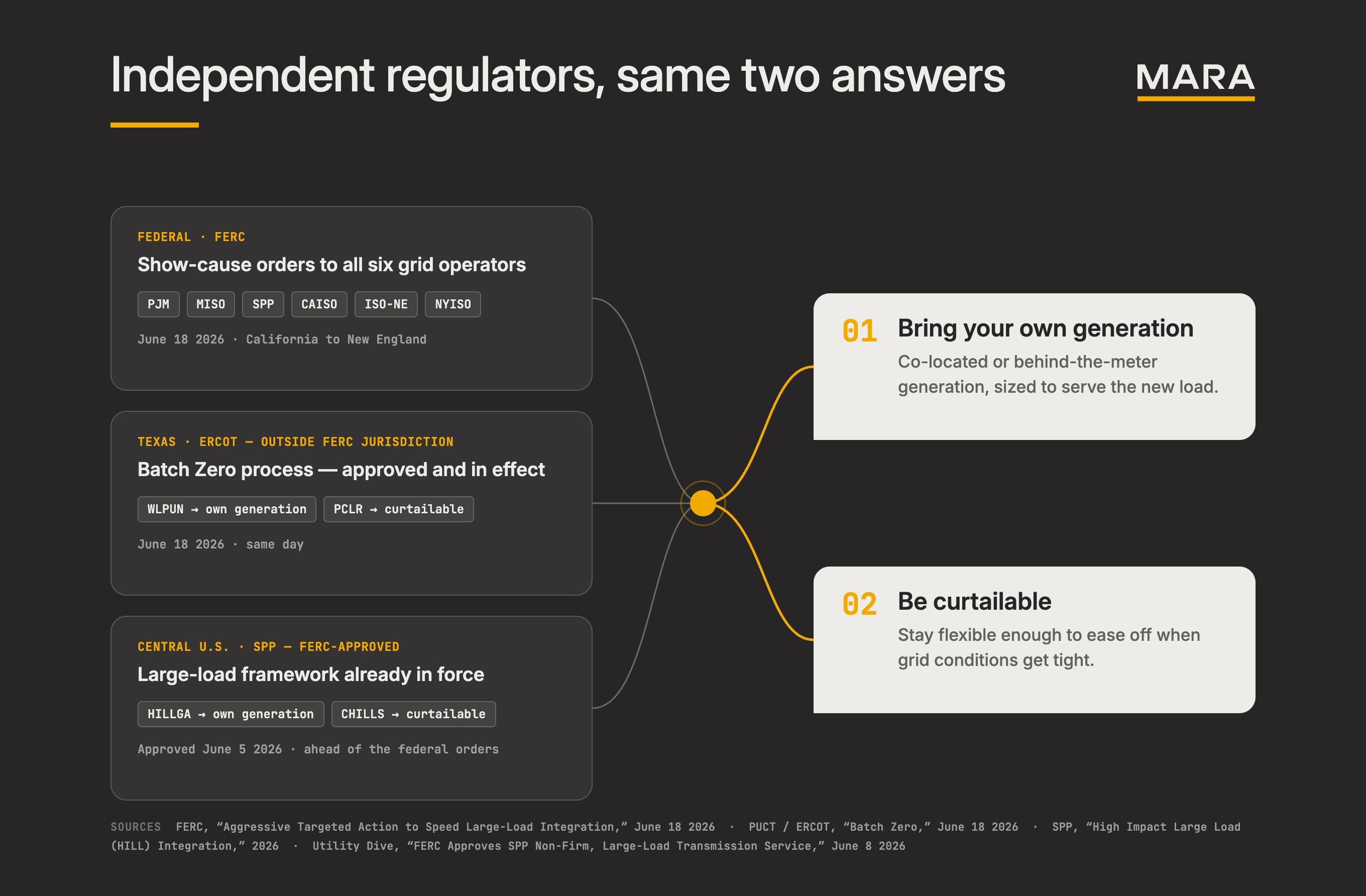

- On June 18, 2026, regulators on separate tracks reached the same conclusion. Two capabilities increasingly matter to integrate new data centers: a load can bring its own generation or stay flexible enough to power down when the grid is tight.

- MARA has run that model for years, at times curtailing more than half a gigawatt when grids are stressed, operating behind its own gas-to-power and wind generation, and pursuing another half a gigawatt of owned generation through its pending Long Ridge acquisition.

- MARA is participating in the policy forums where those rules are taking shape, as a market participant that comments, presents, and testifies from operating experience.

On June 18, 2026, multiple regulators across the U.S. pointed in the same direction about how to absorb the new electricity demand behind the AI boom: large-load interconnection should be redesigned around speed, transparency, and flexibility, with growing emphasis on whether projects can pair new demand with generation or operate flexibly.

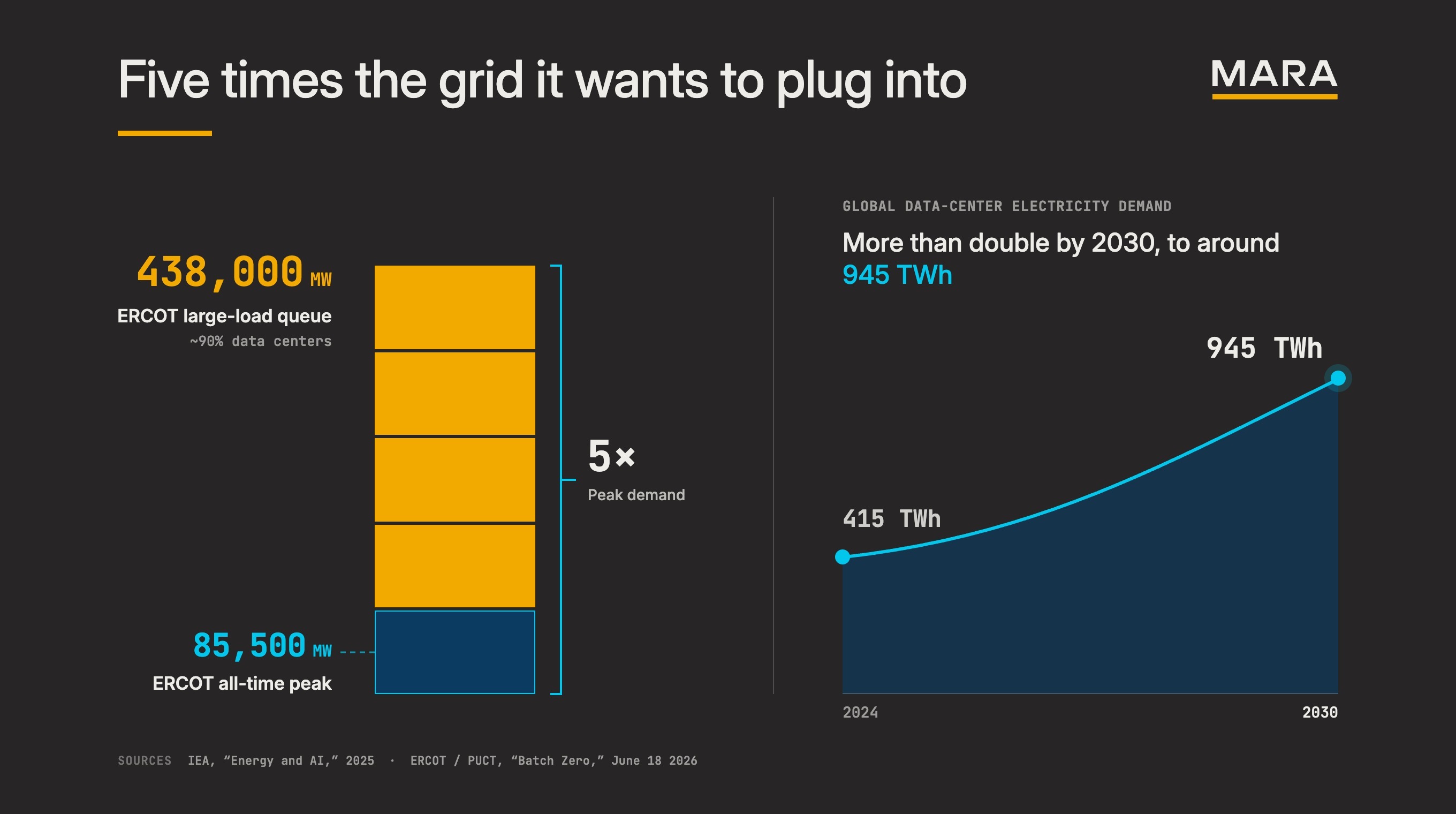

The pressure behind that conclusion is hard to dispute. In Texas alone, the grid operator, ERCOT, is fielding requests to connect more than 438,000 megawatts of new large loads, roughly five times ERCOT’s historical peak demand. Nobody questions that AI demand is exploding. The open question has always been how to absorb it, and regulators continue working to bring additional clarity to the answer.

On the federal side, FERC directed all six grid operators under its jurisdiction to justify or reform their large-load rules across several fronts. Two of those reforms stand out: accommodating co-located, behind-the-meter generation, and creating new transmission services for flexible demand.

The same day, Texas, which runs its own grid outside FERC’s jurisdiction, approved ERCOT’s Batch Zero process, which streamlines interconnection for large new loads, with special provisions for those that bring their own on-site generation or curtail when the local grid is stressed.

SPP, the grid spanning much of the central U.S., is further along still: FERC has already approved its large-load framework, which fast-tracks data centers that pair with their own co-located generation (HILLGA) and those that agree to curtail during grid emergencies (CHILLS).

Federal and state. Coast to coast. The same conclusion. The actions aren't all at the same stage: ERCOT's Batch Zero and SPP's FERC-approved framework are already in effect, while FERC's broader orders to the other operators are just opening the process. But the direction is unmistakable. The fastest ways to connect new large loads without compromising reliability are to pair them with generation or ensure they can operate flexibly.

MARA is not watching that shift from outside. As a registered ERCOT member, and through comments, testimony, and industry forums, MARA participates in the policy conversations where large-load and flexible-load rules are taking shape.

“Testifying before the Ohio Joint Data Center Committee was an important step in establishing MARA as a trusted voice in the state. Every engagement we show up for is an investment in MARA's ability to grow.” - Jayson, SVP of Government Affairs at MARA

Operating Where the Rules Are Headed

MARA has had success operating under both frameworks.

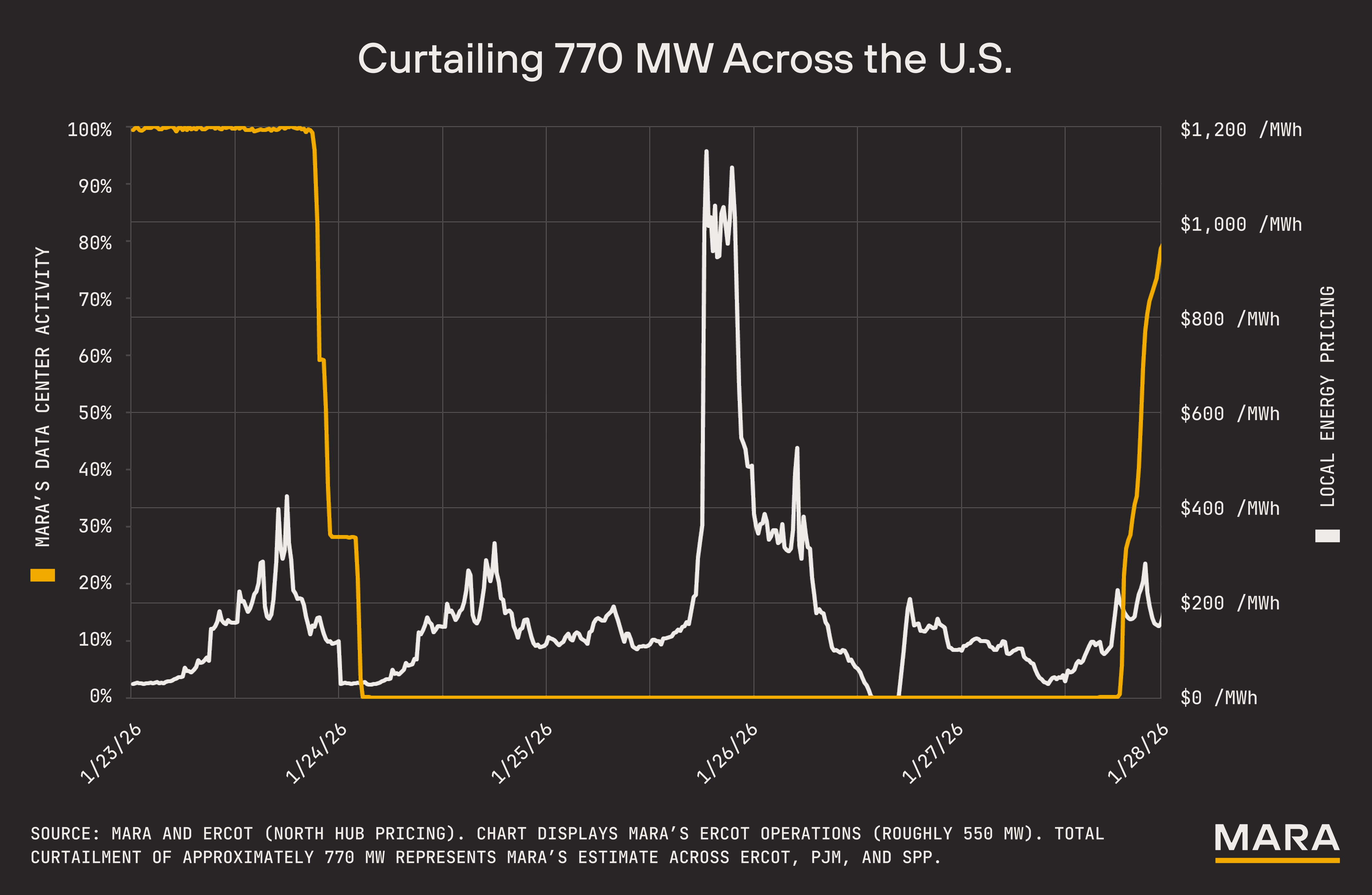

1. Operating Flexibly: MARA is able to monetize electricity when it is abundant and low-cost, then reduce demand when the grid needs that power elsewhere. During Winter Storm Fern in February 2026, MARA voluntarily curtailed roughly 770 megawatts across multiple power markets, including PJM, SPP, and ERCOT, allowing existing generation capacity to serve the grid while under its greatest strain.

This capability is not only useful during energy emergencies. In Ohio, MARA participates in AEP Ohio's coincident-peak program, which rewards large users for reducing demand during the hours of highest system load. While management of coincident peaks is well documented and performed by many large loads, MARA’s level of flexibility allows a more targeted approach to demand side management.

And this is not only for emergencies. MARA curtails when the system needs it, whether demand is peaking or prices are spiking, adjusting its load in a way most large users cannot. In effect, MARA is able to consume power when it is available and to step aside when it is scarce, helping smooth the peaks and valleys that drive volatility in power markets.

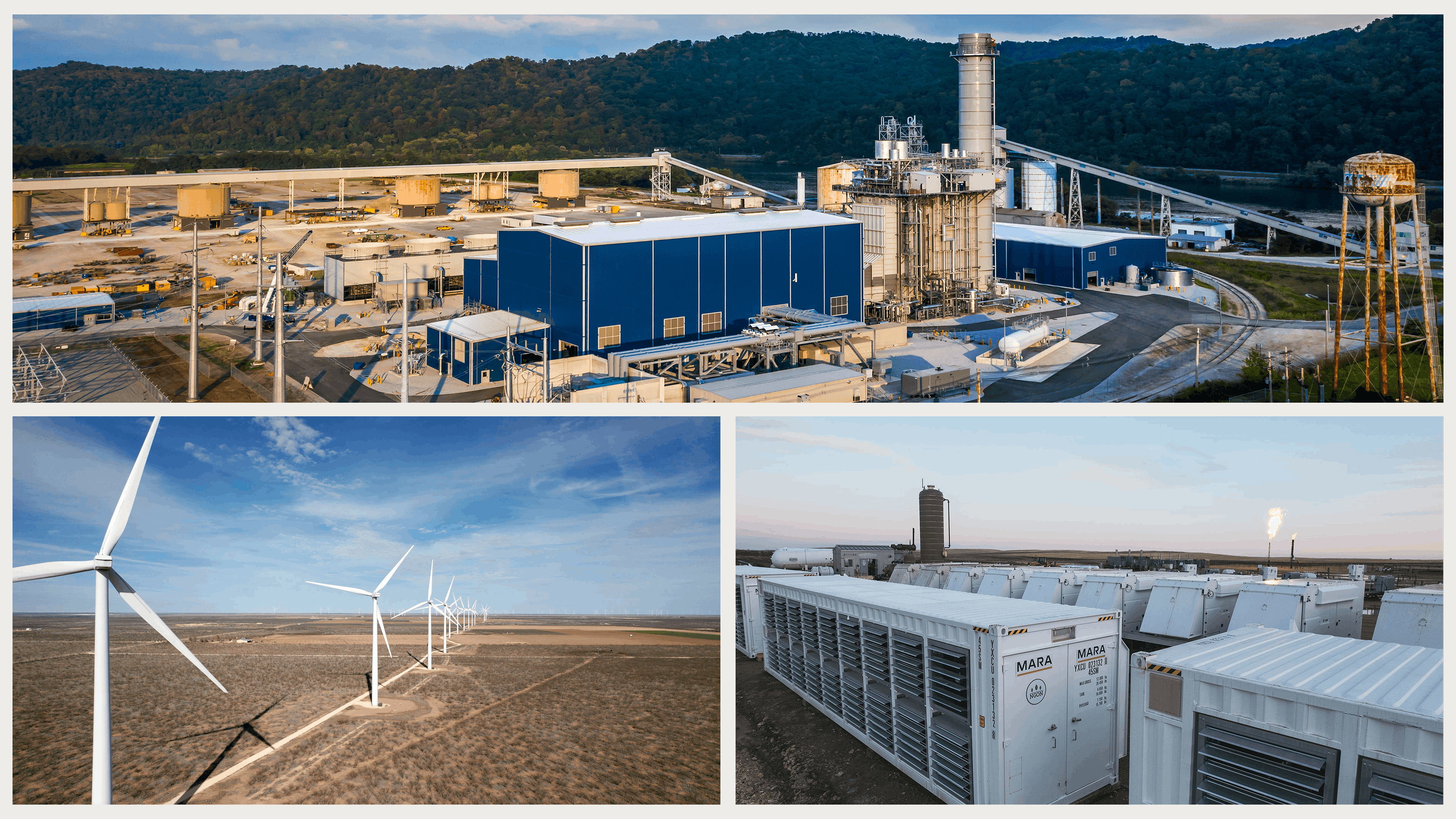

2. Owned Generation: MARA is also expanding its investment in generation that complements its flexible operating model. Through its partnership with NGON, MARA converts stranded and flared natural gas into on-site power, recently doubling capacity to 50 megawatts. MARA also owns a post-PTC wind farm in Texas with 114 megawatts of nameplate capacity, vertically integrating its energy infrastructure stack.

Its agreement to acquire Long Ridge brings an operating natural gas power plant, an existing PJM interconnection, and more than one gigawatt of total campus potential in the long term. Over time, MARA plans to pair new compute demand with new incremental generation capacity at the site.

By acting as a bridge solution for new generation, Bitcoin mining allows MARA to substantially de-risk development projects early in their life cycle. The ability to occupy development sites prior to the arrival of an AI/HPC tenant changes the economics of infrastructure development and create value while longer-term AI and HPC deployment takes shape.

Through strategic partnerships with firms like Starwood Digital Ventures, MARA can pursue powered sites that would otherwise be too capital-intensive or too early in their development cycle for a traditional data center project.

Simply put, we believe Bitcoin mining can enable increased power infrastructure development.

What You Only Learn by Operating

Market rules are changing quickly, and the speed of new demand is accelerating the process. In that environment, experience operating across multiple power markets and technology types matters. It can shape how companies evaluate sites, manage interconnection risk, respond to grid constraints, and turn power access into productive compute.

Flexibility gives large loads a way to work with the grid instead of simply adding pressure to it. Bitcoin mining gives powered sites a productive use while longer-term AI and HPC demand matures. Together, they help bridge the gap between the infrastructure the market needs and the time it takes to develop it.

That gap matters. AI infrastructure is becoming a measure of national competitiveness, and the countries that can bring power, compute, and reliability together fastest will have an advantage. The question is not whether data centers belong on the grid. It is whether they can be built fast enough, and intelligently enough, to support the next generation of American compute infrastructure. MARA is not approaching that future from the outside. It has been building inside it for years.

Forward-Looking Statements

This blog post contains forward-looking statements within the meaning of the federal securities laws. All statements, other than statements of historical fact, included in this press release are forward-looking statements. The words “may,” “will,” “could,” “anticipate,” “expect,” “intend,” “believe,” “continue,” “target” and similar expressions or variations or negatives of these words are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. Such forward-looking statements include, among other things, statements related to the parties’ ability to consummate the Long Ridge acquisition on the proposed terms or on the anticipated timeline, or at all, including risks and uncertainties related to securing the necessary third-party approvals, or the satisfaction of other closing conditions to consummate the transaction; the occurrence of any event, change or other circumstance that could give rise to the termination of the definitive agreement to acquire Long Ridge or any unanticipated difficulties or expenditures relating to the transaction; MARA’s planned development of digital infrastructure projects, including the Hannibal, Ohio campus; the expected capacity, scalability and performance of those facilities; the anticipated ability to shift between hyperscale and AI workloads and Bitcoin mining at those facilities; MARA’s ability to finance the Long Ridge transaction on acceptable terms, or at all; the anticipated benefits of the transaction to MARA, including MARA’s expansion into high-performance computing; MARA’s ability to advance and execute its digital energy infrastructure strategy; the expected earnings and cash flows from Long Ridge and the expected accretive impact of the transaction to MARA’s profitability metrics. Such forward-looking statements are based on management's current expectations about future events as of the date hereof and involve many risks and uncertainties that could cause MARA’s actual results to differ materially from those expressed or implied in these forward-looking statements. Subsequent events and developments, including actual results or changes in MARA’s assumptions, may cause MARA’s views to change. Readers are cautioned not to place undue reliance on such forward-looking statements. All forward-looking statements included herein are expressly qualified in their entirety by these cautionary statements. Actual results may differ materially from those indicated by such forward-looking statements as a result of various important factors, including uncertainties related to market conditions, the risk that the transaction disrupts MARA’s current plans and operations or diverts management's attention from its ongoing business, the effect of the announcement of the transaction on the ability of MARA to retain and hire key personnel and maintain relationships with others with whom it does business, the effect of the announcement of the transaction on MARA’s operating results and business generally and the other factors discussed in the “Risk Factors” section of MARA’s most recent Annual Report on Form 10-K filed with the U.S. Securities and Exchange Commission (the “SEC”) and the risks described in other filings that MARA may make from time to time with the SEC. Any forward-looking statements contained in this press release speak only as of the date hereof, and MARA specifically disclaims any obligation to update any forward-looking statement, whether as a result of new information, future events, or otherwise, except to the extent required by applicable law.

MARA Company Contact:

Telephone: 800-804-1690

Email: ir@mara.com

MARA Media Contact:

Email: mara-jf@joelefrank.com

* Currently authorized to sell 485 MW; expected to increase to full 505 MW nameplate in H2 2026.

.png)